Hsmb Advisory Llc Things To Know Before You Buy

Hsmb Advisory Llc Things To Know Before You Buy

Blog Article

Not known Details About Hsmb Advisory Llc

Table of ContentsUnknown Facts About Hsmb Advisory LlcExcitement About Hsmb Advisory LlcLittle Known Facts About Hsmb Advisory Llc.Hsmb Advisory Llc for DummiesHow Hsmb Advisory Llc can Save You Time, Stress, and Money.What Does Hsmb Advisory Llc Do?

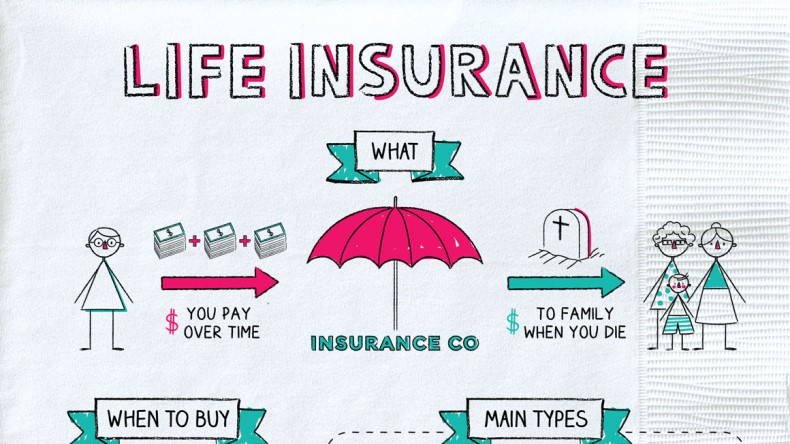

Ford states to avoid "money worth or permanent" life insurance policy, which is more of an investment than an insurance policy. "Those are very made complex, included high payments, and 9 out of 10 people don't require them. They're oversold because insurance agents make the biggest payments on these," he states.

Handicap insurance policy can be pricey. And for those that choose for lasting treatment insurance coverage, this policy might make disability insurance unneeded.

Top Guidelines Of Hsmb Advisory Llc

If you have a chronic health problem, this type of insurance coverage can end up being vital (Life Insurance St Petersburg, FL). Don't allow it stress you or your bank account early in lifeit's usually best to take out a plan in your 50s or 60s with the expectancy that you will not be using it till your 70s or later on.

If you're a small-business proprietor, think about securing your income by acquiring company insurance. In the event of a disaster-related closure or duration of rebuilding, business insurance policy can cover your earnings loss. Think about if a substantial weather condition occasion affected your storefront or production facilityhow would certainly that impact your earnings?

And also, utilizing insurance coverage could occasionally set you back even more than it saves in the long run. If you obtain a chip in your windscreen, you might take into consideration covering the repair expenditure with your emergency situation cost savings rather of your automobile insurance. St Petersburg, FL Health Insurance.

Fascination About Hsmb Advisory Llc

Share these pointers to shield loved ones from being both underinsured and overinsuredand speak with a relied on specialist when needed. (https://issuu.com/hsmbadvisory)

Insurance that is purchased by a private for single-person insurance coverage or protection of a family. The private pays the costs, as opposed to employer-based medical insurance where the company frequently pays a share of the premium. People might shop for and purchase insurance policy from any kind of strategies available in the person's geographic region.

People and households might get monetary aid to reduce the cost of insurance costs and out-of-pocket costs, but only when signing up through Attach for Health Colorado. If you experience specific modifications in your life,, you are eligible for a 60-day amount of time where you can register in an individual strategy, also if it is beyond the yearly open registration duration of Nov.

Hsmb Advisory Llc for Beginners

- Connect for Health And Wellness Colorado has a full checklist of these Qualifying Life Events. Reliant kids that are under age 26 are eligible to be consisted of as member of the family under a moms and dad's insurance coverage.

It may seem simple yet comprehending insurance policy kinds can likewise be perplexing. Much of this confusion comes from the insurance policy market's ongoing goal to make individualized coverage for policyholders. In creating versatile policies, there are a selection to pick fromand every one of those insurance policy types can make it difficult to recognize what a particular plan is and does.Hsmb Advisory Llc Can Be Fun For Anyone

The most effective place to start is to discuss the difference in between the 2 types of fundamental life insurance coverage: term life insurance coverage and irreversible life insurance coverage. Term life insurance policy is life insurance policy that is only energetic for a while duration. If you die during this duration, the individual or individuals you've called as beneficiaries might get the cash money payout of the plan.

However, several term life insurance policy policies allow you convert them to an entire life insurance plan, so you don't lose insurance coverage. Typically, term life insurance policy plan premium payments (what you pay each month or year into your policy) are not secured at the time of purchase, so every five or ten years you have the plan, your premiums might rise.

They additionally tend to be less costly general than whole life, unless you acquire an entire life insurance coverage plan when you're young. There are additionally a couple of variants navigate to this website on term life insurance policy. One, called team term life insurance policy, is usual amongst insurance policy alternatives you could have access to via your employer.Some Ideas on Hsmb Advisory Llc You Should Know

This is commonly done at no charge to the employee, with the capacity to buy extra coverage that's gotten of the staff member's paycheck. An additional variation that you could have access to through your employer is supplemental life insurance policy (Health Insurance). Supplemental life insurance policy could consist of accidental fatality and dismemberment (AD&D) insurance coverage, or burial insuranceadditional insurance coverage that could assist your family members in case something unexpected happens to you.

Permanent life insurance simply describes any life insurance policy that doesn't expire. There are a number of types of long-term life insurancethe most typical types being whole life insurance policy and universal life insurance policy. Whole life insurance policy is specifically what it sounds like: life insurance coverage for your whole life that pays to your recipients when you pass away.

Report this page